I subscribe to many credit tracking apps, most of which are free but none have been as responsive as WalletHub. Both credit card issuers and consumers make genuine mistakes but just because it may have been an error, doesn’t mean that it is consequence free. This is not a sponsored post, but I have had a good experience with WalletHub, they saved my credit from disaster!

If you are considering booking travel or signing up for a new credit card please click here. Both support LiveAndLetsFly.com.

If you haven’t followed us on Facebook or Instagram, add us today.

What happened?

Credit is vital to my travel experience as it ensures that I am able to get approval for new cards (and the bonuses that come with them). It also helps me keep my interest rates low on conventional loans and maintain my general financial health. I subscribe to a number of apps and services which I will cover shortly, among them, CreditKarma, Credit Sesame, Credit Wise, and WalletHub.

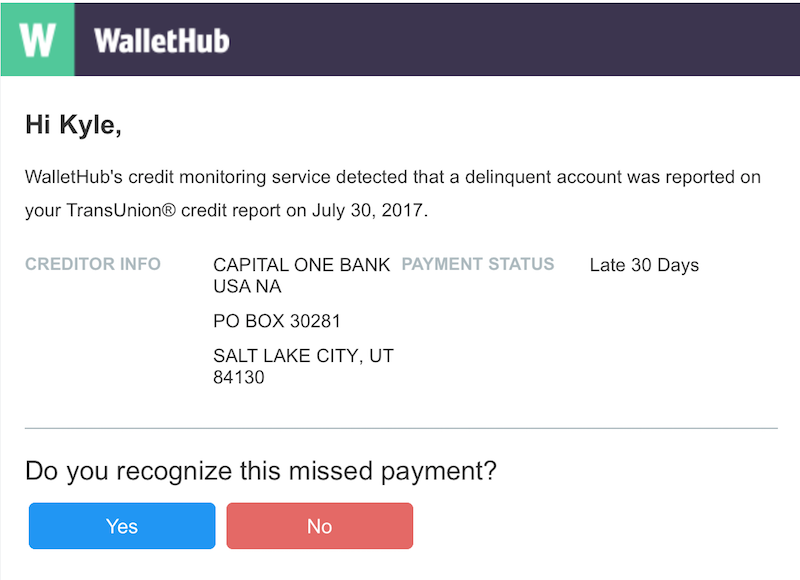

Earlier this week I woke up to an email from WalletHub asking if I was aware of a 30-day late notice posting to my credit report. Wait, what? There is a clickable link within the email that asks if this is valid or not and then has an option to start a dispute. While missing a payment by 30 days is surely an unthinkable reporting error, I thought to call the bank in question first and see if it was valid, despite how unlikely it seemed.

It turns out that when I closed a card a couple of months ago, though I had no balance at the time, a charge was allowed to be processed after I had asked for the card to be closed and before it actually was closed. I received no documentation from this in the mail, electronically in an email – not even a single phone call even to try to get me to pay my bill.

This is unconscionable. Subsequently, I intend to terminate the rest of my relationship with Capital One when it makes sense to do so.

I called in to get the matter resolved, paid the charge in full and was told that not only would it be properly closed this time, but they would waive the associated fees and interest as a one-time courtesy. That suits me because it will be the last time we do business. They also indicated they will correct my report but it may take up to a month to come off as a late payment. I could have disputed the charge, but the amount was small and I didn’t want to drag it out.

WalletHub was the first service that alerted me to this by more than 12 hours. I logged into my other services to confirm the validity of the issue and none of the others even knew it existed.

I subscribe to a paid service with Credit Sesame and despite them reaching out with marketing offers and to tell me I had recently been hit with a credit pull (I applied for a card) – they didn’t let me know about this huge issue on my report until much later. I am also considering pulling my paid service from Credit Sesame as a result. In the days since the missed payment was reported Credit Sesame has let me know just shy of a dozen times, which would have been helpful if I didn’t have WalletHub, but since I do, it was more annoying than anything else. Credit Sesame has used each of these notifications (in the app, through emails, and various other notification tools) to draw me to login and pay for more services.

Alternatives

WalletHub is a free service but they are not alone in this space. Credit Sesame and Credit Karma both offer basic credit tracking and a Vantage score (a composite estimate of your actual score) as does WalletHub. All three of their business models are built around helping consumers better manage their credit as a free service in the hopes that they will pursue their new credit cards on their site, earning them a commission for their efforts.

Credit Wise is offered by Capital One and offers a stripped down version of the others but it’s terrible. Considering that it is offered by Capital One, the offending bank, it’s surprising they didn’t alert me through the process and only finally notified me after Credit Sesame. I had resolved the matter minutes after receiving the notice from WalletHub.

Credit Karma sent me nothing for two days. It was just a single email with the same dispute offer as WalletHub. I took them up on their dispute process which led me to a phone number where I filed a claim. I may write about that in the future if there is more of the story to tell.

Credit Sesame offers a paid version for $9.99/month that gives some further identity protection but I mostly use it for the three bureau credit report they offer, available for full download monthly. I will be keeping this through the next couple of months to make sure the late payment comes off all of my bureaus and carry out any discrepancies with them before determining if they deserve my future business.

Discover Card offers some light reporting for free even to those that are not Discover card holders, but I don’t use their service so I can neither endorse nor disparage their product.

Which Should You Use?

All of them. WalletHub was the one that caught this issue fastest. Credit Karma missed my recent application and hard credit pull as did all the other services other than Credit Sesame, the only one who caught it. By having all three, I have a better picture of the bureaus by combining the Credit Karma and Credit Sesame Vantage scores and more or less ball-parking the number form there. WalletHub is Johnny-on-the-spot with fast alerts that saved my bacon this go around.

They all offer a free service so why not have them all?

The only one I will likely drop is Credit Wise by Capital One which has proven completely useless as is the bank itself.

Have you tried WalletHub? Have you found their alerts to be better than CreditKarma or Credit Sesame? Do you have any recommendations for alternative services?

Leave a Reply