A new startup, Level Skies, promises to provides price protection for your next airline trip. You enter your trip details and how long you wish to lock in the best price guarantee (between 1 to 4 weeks). They then search for airfare and calculate a fee to protect you in case the price increases during this time. The “locked in” price is the lowest currently available fare in the market–not necessarily the specific flights you want. If you choose to pay their fee, you can sit back over the 1-4 week period and see if the price decreases. If it does not, you can purchase your airfare and if the lowest fare has gone up, Level Skies will refund the difference between the lowest fare when you locked in their service and the lowest fare on the day of purchasing your ticket.

A new startup, Level Skies, promises to provides price protection for your next airline trip. You enter your trip details and how long you wish to lock in the best price guarantee (between 1 to 4 weeks). They then search for airfare and calculate a fee to protect you in case the price increases during this time. The “locked in” price is the lowest currently available fare in the market–not necessarily the specific flights you want. If you choose to pay their fee, you can sit back over the 1-4 week period and see if the price decreases. If it does not, you can purchase your airfare and if the lowest fare has gone up, Level Skies will refund the difference between the lowest fare when you locked in their service and the lowest fare on the day of purchasing your ticket.

It sounds like a promising concept, but the website is a bit vague, so I reached out to Chris at Level Skies with some questions:

The basic idea is that we are paying you for “insurance” that the lowest price for our trip will still be the lowest price in one to four weeks?

That’s right, if the price between your locked-in fare and the lowest ticket price that matches your lock-in travel preferences goes up, we’ll pay you the difference. Keep in mind, with us you are not locking in the price of a specific flight, but rather assuring yourself that a flight will always be available for your trip for the price you lock-in. However, you don’t have to take that lowest fare flight if you don’t want to. With our system, we’re totally okay with our customers booking whatever flight they prefer, and booking through whatever ticket seller they like – regardless of the flight they take, we’ll still pay them the difference between their locked-in fare and the lowest fare flight of the day they book. All they have to do is send us their booking confirmation email and we’ll cut them a check.

For example, lets say John wants to go to L.A. from S.F. on June 10th or 11th and return on the 15th. For a $10 Flex Fare, he can lock in the price of the cheapest ticket for those days on that route for a month. Lets say that roundtrip ticket is $200 at the time John buys the Flex Fare. Within that month, he decides to wants to travel on the 10th and so he comes back to Level Skies and sees that the lowest fares on the 10th have gone up to $230 (we also send emails on a regular basis to give this information); so his pay-out if he does book a ticket is $30. Lets say John likes to fly Main Cabin Select on Virgin – but that ticket price is $250 when he books it. That’s not a problem – we’ll refund him the $30 no matter what ticket he buys. So long as his booked ticket matches the route and dates of his Flex Fare, we’ll send him the check.

If the prices goes down, do you keep the fee that was paid?

That’s right, if prices go down then we still keep the fee we’ve charged – that’s how we can provide peace-of-mind to all our customers. However, if the fare has gone up in our data system (we get our data from one of many ticket price providers, not all of which match each other) but the customer is able to find a ticket for less elsewhere, we’ll still pay out the difference between the lock-in price and the lowest fare in our system.

If the customer decides not to book do you keep the fee?

That’s right, if the customer never books the flight, then we can’t refund the fee for our price protection.

Can the insurance be extended?

Our price protection service is valid for 1, 2, 3, or 4 weeks, which the user decides at time of purchase, but we don’t currently allow customers to extend that time period after purchase. We are actually considering this extra time-extension functionality right now, but as it stands today, once the purchase is made, the decision time is set, and once the decision time has expired the price protection ends.

* * *

Note that this service is not available out of all airports right now. In fact, it is limited to flights from the following hubs–

- Atlanta, GA – Hartsfield-Jackson Airport (ATL)

- Boston, MA – Logan International (BOS)

- Chicago, IL – O’Hare International (ORD)

- Dallas, TX – Dallas-Fort Worth Airport (DFW)

- Los Angeles, CA – Los Angeles Airport (LAX)

- New York, NY – JFK Airport (JFK)

- Philadelphia, PA – Philadelphia Airport (PHL)

- San Diego, CA – San Diego International (SAN)

- San Francisco, CA – San Francisco Airport (SFO)

- Washington, DC – Dulles Airport (IAD)

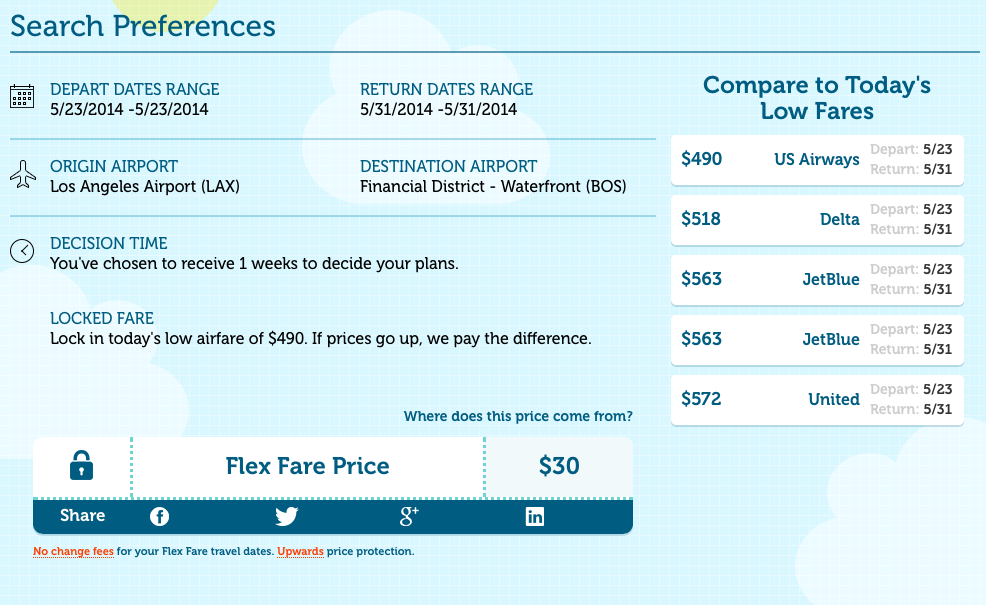

Taking it for a test drive, I searched for a trip to Boston in three weeks, choosing to hold the fare for one week. The search returned the following –

A downside I see is that fares tend to vary based on time of day and you cannot lock in a preferred departure time (regardless of airline). So you may be eyeing a specific flight itinerary and find it shoots way up during the insurance period but you will receive no compensation if you end up spending $200 more for that flight if a far-less-desirable itinerary is available for the “insured” price.

Also, I would like to see the search engine will better identify (or filter) codeshare flights. Looking above at option two for $518, it appears that Alaska operates a non-stop flight from BOS to LAX. It does not: that is an AA codeshare. Not a big deal to most, perhaps, but I like to know which carrier is being shown for the price comparison. Even when I click on “show details” it still does not identify the operating carrier:

It seems the search engine constrains searches to one or two stops, so if you are totally flexible on your travel, this may be a money-saving tool for you. I prefer United’s FareLock system because it allows me to reserve the specific Untied flights I wish for about the same price, but since other carriers do not have a similar system, or if you are carrier agnostic and are simply looking for the best price, this tool can be useful.

Since you have a connection at Level Skies I would inform them that not displaying the code share details will quickly land them in hot water with the DOT. They’ll be subject to significant fines, detrimental to a startup like this. Several high profiles OTAs and airlines have been hit with these over code share violations.

@Chase: I mentioned it to them already and will forward them your comment.

Seems like a complicated insurance product which is best avoided.