A slurry of new “buy now, pay later” apps have the potential to change the way we travel.

If you are considering booking travel or signing up for a new credit card please click here. Both support LiveAndLetsFly.com.

If you haven’t followed us on Facebook or Instagram, add us today.

Buy Now Pay Later Apps

A number of new “Buy now, pay later” apps have hit the market over the last two years but are hitting their stride now. Klarna is one that utilized a Super Bowl commercial to introduce new customers to the market, Affirm is another. AfterPay, an Australian firm, was just bought as the largest transaction in the country’s history when Square offered $29bn to integrate into the company’s Cash app.

I am going to focus most on Affirm for the purposes of this piece.

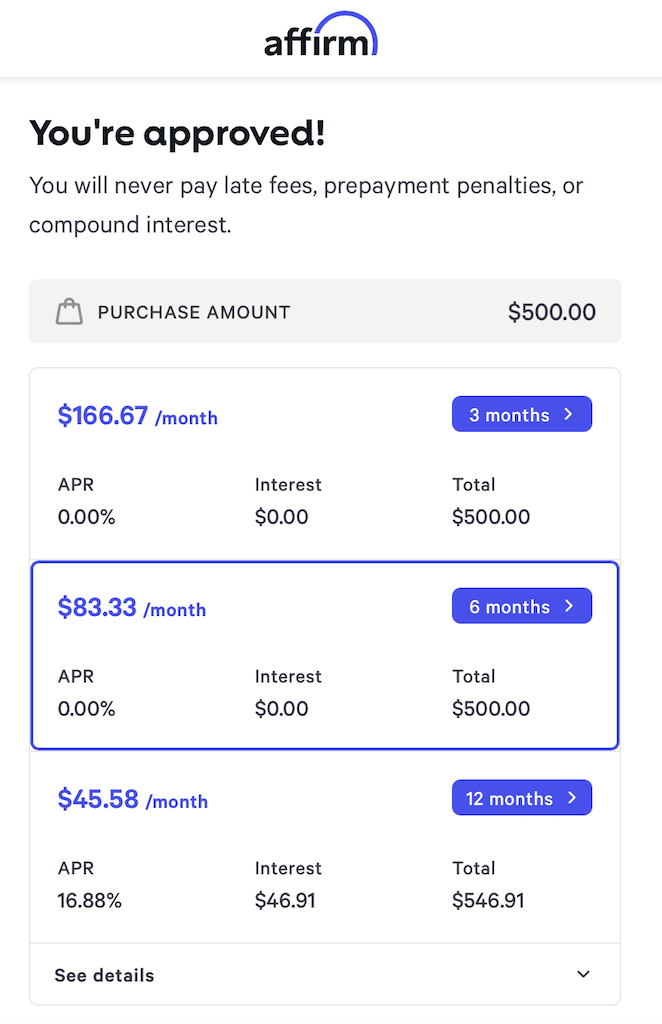

The key advantage of Affirm’s “buy now, pay later”: no credit check. This goes for the competition as well along with transparency in what will be charged, when and where. More and more fintech firms are shirking the traditional credit score in favor of a soft pull to verify the identity and then cross-referencing that with limited data to determine financial ability to repay.

This is ideal for both those with good and bad credit. The Klarna app, and others like it, offers interest-free payment plans for the purchase amount in installment payments. Depending on a consumer’s financial worthiness, the amount offered and the term to pay it off will vary but generally speaking, 6-12 weeks are standard free windows, though it will also vary by retailer.

Interest rates do apply for longer loan terms ranging from 0-30% though most I have seen offer 3-6 months interest-free monthly payments, and at 9-12 months, the interest rate applies. This is not a revolving credit line, it’s a micro-loan for a single transaction that earns its customer’s trust by avoiding hidden fees, and keeping spending limits manageable.

My limit was lower than any credit card I have ever applied for so its usability for me is pretty limited. However, for purchases I don’t want to make but have to, this could be a nice stand in.

How Does It Work?

These apps are working both sides of the transaction. They receive both a commission from the retailer and interest from the consumer when they choose to finance beyond free installments. An app like Affirm will pay for purchases on terms established with the retailer (60-90 days – just a guess) all the while the consumer is making payments to the lender, those who extend beyond the payment terms the app has with the retailer incurs interest.

Some retailers who are looking to promote larger purchases will offer longer terms interest-free or lower rates. The interest, when charged, is a flat rate, not compounding.

With a more direct payment history and as loan installments are withdrawn from a checking account, the app may be able to make more intelligent lending decisions on a borrower by borrower basis without requiring the use of a loan officer.

Travel Companies Participating

Travel companies are a great fit for this type of application in theory. They are larger ticket items that consumers may hold off on purchasing until they are ready to pay all at once, but prices change and the sale may be lost. For many consumers, it’s far easier to absorb payments than bulk purchases and credit cards give just 30 days to avoid high-interest rates.

Here are some of the travel companies participating with Affirm (though the list is not necessarily complete):

- Travelocity

- Orbitz

- United Airlines

- Delta Vacations

- Hotels.com

- VRBO

- Expedia

- American Airlines

- Frontier Airlines

- Hotwire

- Southwest Airlines

- Priceline

- RV Share

- Cheap-o Air

- AirBnB

There’s also an option to use a virtual credit card (utilizing your available credit) to buy at a retailer not listed in the system.

One advantage travel agents have long held over direct-to-consumer online sales is the ability offer payments for a trip over time. A deposit is taken at the time of booking, then easy monthly payments allow consumers who would struggle to save $2,000 for the cruise they really want, but at $200 down, and $150/month, it’s something they can easily afford.

That can really change travel by opening the doors to new consumers. It also makes it easier to spend a little more money on bookings. Southwest famously succeeded not by competing with major airlines, but with driving. In essence, they were bringing in new consumers instead of trying to take marketshare from the existing market. This feels like that.

Competition From The Banks

American Express has a couple of options for installment repayment terms: Plan It, and Pay Over Time. Plan It is the most like these systems by establishing fixed payments at the time of purchase but Plan It will have a fee based on the duration of the note anywhere from 0-30%. I was recently offered 10%, in the past, I have seen it as low as 0% and 4-7%.

Chase also offers a fixed pay-over-time option for some credit customers with no fees, and no interest (assuming payments are made on time and in full as due) but that’s a limited offer and will not stay in place for a lasting period of time.

Every month, my house receives checks from credit cards we don’t use offering balance transfer or fixed payment offers for 0-3% and terms of 12-18 months. We occasionally take the banks up on these because the credit line is already established, and for zero or very little interest, I would always rather keep my cash on hand.

What I dislike about those deals are the “gotcha” terms. If it’s not fully paid back within the term, it incurs a max interest rate for the entire period (for which I would have been better off just charging it on my card and paying back at normal interest rates.) It also disables that card for me as I don’t want to do the monthly math to ensure that my installment amount and my normal charges are paid without paying off the balance of the financed amount early.

The problem for new consumers, for which travelers are some of the most often targeted, is that they do not want a hit on their credit and even these small balance transfers will affect your credit score as utilization will increase. Installment loans are viewed differently and Affirm and others will report payments to the bureaus. That helps new credit applicants build their credit but without requiring a hard credit pull to establish it in the first place.

Will I Use It?

If the expenditure is significant, this might be a nice alternative. As I mentioned, I always prefer to hold onto cash and finance for free if possible. I am going to try it out on some small purchases to see how it works and if it’s a good fit for me and my family. I know others that will use this for travel purchases already, and it makes trips possible that might have otherwise remained out of reach.

What do you think? Have you tried these apps? Will you consider them or use your own financing instead?

Nice explanation. We just ran a story on some of the fraud problems with BNPL. https://www.f5.com/labs/articles/cisotociso/fraud-scenarios-in-the-buy-now-pay-later-ecosystem

Back in the 50s and 60s the major airlines directly offered financing plans like ‘low interest for 24 months’ for leisure travelers – airfare was a large expense vs everyday items back then. AA called it the american airlines personal credit plan.

This ‘BNPL’ is just a bunch of hype of a the second oldest business model – lending

Hart to take this seriously when you don’t even mention the first google result for Travel Finance.

Uplift doesn’t offer an app so that’s pretty much a non-starter for a post about “Buy now, pay later” apps.

It also won’t change travel because:

• Uplift doesn’t offer anything outside of travel (https://www.uplift.com/find-partners/). That won’t bring new customers into the fold.

• They charge interest

• They require a credit check

“ Kyle is a freelance travel writer with contributions to Time, the Washington Post, MSNBC, Yahoo!, Reuters, Huffington Post, MapHappy, Live And Lets Fly and many other media outlets”

Since it appears you only write for liberal publications it’s hard to take anything you post seriously. Are you willing to admit you are a liberal? It would make it easier for readers to understand where you are coming from with anything you post.

Sadly this is the world we live in. You lose 50% of the audience when you accept the stuff HuffPost puts out there by contributing to them.

Yep, Kyle is a bleeding heart liberal. He follows in the footsteps of other great liberals like Mussolini and Mitch McConnell in that they fueled the left-wing media machine by writing for MapHappy.

“Dave Edwards” clearly has no clue and hasn’t been coming to this site on Sundays for the articles

Sounds like something Spirit travelers would fall for.

Never ever underestimate the ability of new businesses to F morons.

And we the good people of Florida appreciate suckers spending money they don’t have to visit us. It’s keeps our state income tax level at zero. By the way, what are the rates in New York and California?

Florida resident (probably of The Villages)…all clear now

Funny how all the NYCers who moved to Florida last year seem to realize…all the downsides of Florida and have come back. NYC is booming.

Sounds pretty sweet at first, doesn’t it? No credit pull, great terms as long as everything goes perfectly, and you get to pay over time. Harken back around 13-14 years ago when even huge financial institutions like Citi were at death’s door and you’ll get an inkling of where things are headed when we hit another major recession. Then again I may be mistaken.