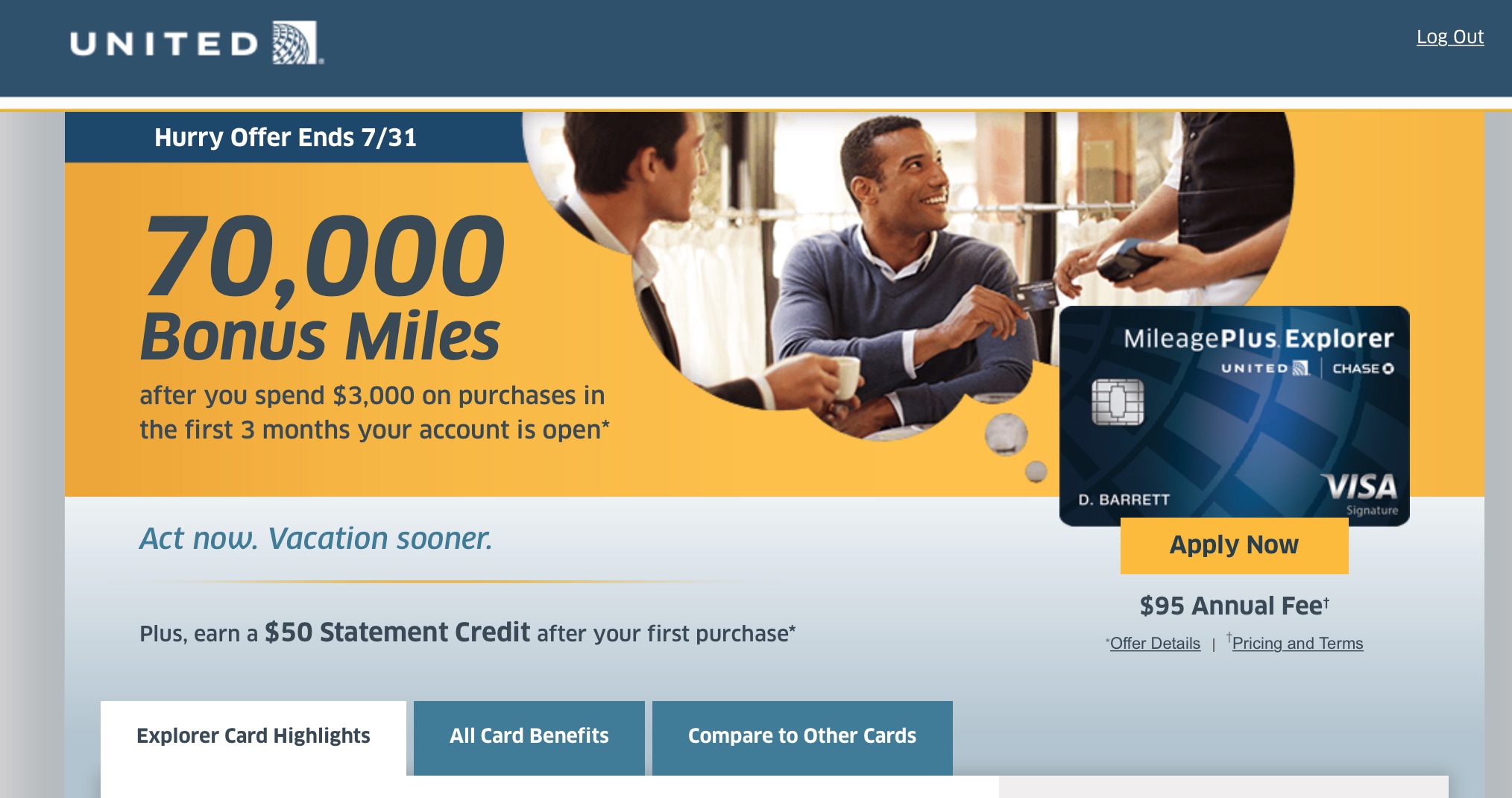

Last week I wrote a post entitled My Final Credit Card Churn for Two Years. I mentioned that even though I was over 5/24, I applied for the Chase MileagePlus Explorer Card, essentially just to confirm I was over the limit. Turns out, I was approved.

I never received a call from Chase, still have not received the card in the mail, but the card now shows up on my Chase online account with a fairly substantial credit line. Interestingly, Chase pulled the credit from Chase Sapphire Preferred card. Usually Chase calls to discuss this before taking action, but either I missed it the call or someone just took matters into her own hands.

How Did I Get Approved?

I consider myself an expert on miles and points, but not credit cards. I cannot figure how I was approved for this card when I have applied for the following cards over the last two years:

- Starwood Preferred Guest Credit Card

- Chase Sapphire Reserve Credit Card

- Citi / AAdvantage Executive World Elite Credit Card

- Alaska Airlines Visa Signature® Credit Card x 2

I’ve also applied for the following business cards, which do not seem to account against 5/24:

- AmEx Blue Business Plus Credit Card

- Starwood Preferred Guest Business Credit Card

- Chase INK Preferred

I am assuming now, after my flurry of applications, that I cannot sign-up for another 5/24 Chase card for the time being.

But I remain curious how I got approved in the first place.

Just another data point…

Most business cards do not report to your personal credit report and therefore don’t count. Most reports I’ve seen indicate that even Chase business cards do NOT count towards your 5 card limit

What a piece of click-bait. If you really don’t know the rules of 5/24, then I guess we have to take your advice with a grain of salt.

My knowledge is in airline and hotel loyalty and mileage redemptions, as I prefaced this post by saying. But thanks for taking the time to comment…

Have you checked which personal cards show up on credit report they actually pulled? You might be 5/24 on your own count but Experian, TransUnion, etc., might only have you at 3/24 (or one has you at 3/24 the other at 5/24 but they pulled the on at 3/24). I know my count differs between the credit agencies.

All I know is that this was my sixth card (and Hyatt my seventh).

I see three possibilities:

– one of your credit cards is actually older than 24 months

– one of your credit cards is very recent, and doesn’t show up on your credit report yet. In particular, amex usually only reports cards after the second statemnent. I suggest you look at your credit report on the three bureaus (TU and EQ on creditkarma, EX on their own website/app) and see if you are in that situation (or the previous one).

– you just got very lucky 😉

Or United had talked to Chase, Scott Kirby told me they were not happy with their credit card portfolio and that they may need to change that rule to grow the portfolio again.

Seriously, go to Credit Karma and look at your actual credit report and see what new accounts show up from within the last 24 months. And then you can figure out how you didn’t really beat 5/24 instead of just wondering what happened.

I beg to differ with some of the above comments. My 2 Chase Ink cards, and my B of A Alaska Business were counted on my “5/24” based on my reconsideration calls.

Matt, (and anyone who might want to chime in) may I ask for your opinion? I will be off the “5/24 purgatory” in about 48 hours, and, curiously, am becoming less excited about the Chase Sapphire Reserve, especially based upon Gary Leff’s piece that speculates whether Chase will cut back on the benefits on the CSR. I am also eligible for the Business Explorer with the bonus. Any input will be greatly appreciated.