The US affinity credit card market is excellent for brands and for banks. Several offer excellent bonuses, yet the Japanese carriers are woefully inadequate and offer more points indirectly than directly. What’s wrong with them?

If you are considering booking travel or signing up for a new credit card please click here. Both support LiveAndLetsFly.com.

If you haven’t followed us on Facebook or Instagram, add us today.

***Live And Let’s Fly writers are not paid a commission by credit card issuers and our opinions are solely our own. Many peer bloggers do receive a commission from credit card sign-ups and if you decide you would like to pursue one of the cards I mention, try their site before going straight to the issuer.***

Bonuses Are So Bad

Gary Leff writes occasionally about the signup offers from Japan Airlines (JAL) credit card offers in the US. The last one I recall incentivized would-be cardholders with a stuffed animal-style airplane. Seriously. ANA has a huge bonus out for their card right now. Prepare yourself.

You can earn 5,000 ANA miles when you open a new card and spend on your first purchase.

5,000.

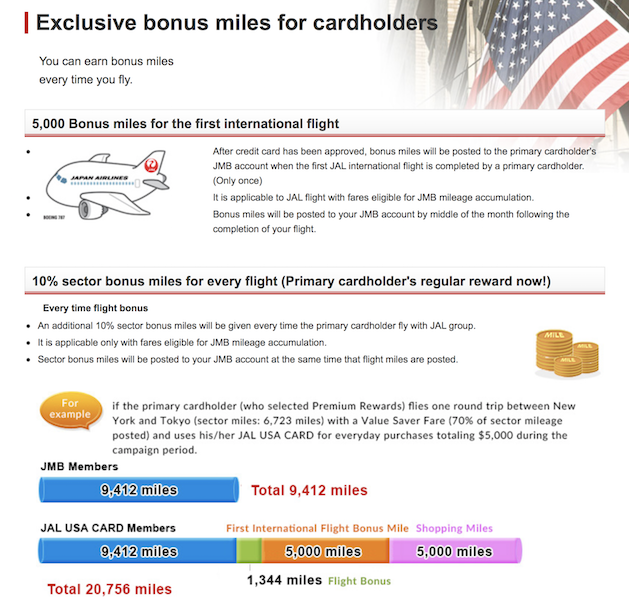

That’s enough points… for nothing. Don’t lose sleep dreaming of all the place you can go when you finally cross 11,000 points, the minimum redemption value. Not to be outdone, JAL matches the offer, but, with a caveat naturally. To receive your 5,000 JAL Mileage Bank miles you need to fly JAL on an international ticket and presumably, that will be trans-Pacific given that this card is for the US-only.

By comparison, the American Airlines Citi card or the Aviator from Barclays both offer enough miles on their signup bonus for a round trip to Japan in coach – on Japan Airlines (no less) if you would like. On the JAL Card website, they map how to achieve 20,756 miles. In order to beat the normal rate of any JAL Mileage Bank member you would need to take the flight, get the one time bonus, plus a 10% and spend $5,000 on the card. Doing all of that will earn you enough points to upgrade one-way trans-Pacifically from Economy to Premium Economy.

But wait, there’s more!

For a limited time, the JAL card offers… 10,000 bonus points for spending on the card. How much you ask? Great question, $5,000, or two miles per dollar spent. If you spent $15,000 during the promotion you would have enough to get a return upgrade from coach to… premium economy – on a paid ticket. That is to say, you would need to both spend the $15k and buy a coach ticket you hope to upgrade to premium economy in cash. By comparison, similar spending (with the international ticket, sign up bonus, spending bonus) could net JAL flyers with the American card a business class one way and coach return, and wouldn’t require you to buy the coach ticket.

Is it Japanese Custom?

Some may speculate that the crazy high US credit card bonuses run counter culture to Japanese customs and that should explain the disparity. While there may be some merit to differences in approach, I tend to believe it’s not the primary driver in holding back bonuses from making either card one worth having.

Cathay Pacific has a US affinity card that recently re-vamped to increase its bonus and put themselves on the map. Korean partners with US Bank and achieves a reasonable 20,000-40,000 points (depending on when you sign up), completely respectable in my eyes from a small national bank (comparatively) and in line with other foreign carriers. While Japanese culture is entirely different from Cantonese or Korean, the carriers are not adverse to selling their miles through other resellers including other banks. By coincidence, I found a very high bonus for Cathay Pacific’s Asia Miles credit card while in Hong Kong recently which demonstrates to me that big bonuses may not be limited to the US market.

It Is The Partner Bank’s Fault?

First National Bank of Omaha is small (nationally), I should know. Originally from Omaha, I used the bank for many years and if you live in Omaha or Nebraska generally – they are the bank of choice. They have spread their footprint to some other locations in Dallas and Denver, mostly through acquisitions and because of Omaha connections nearby, but JP Morgan Chase they are not.

This is where I feel like some if not all of the blame rests. It’s not that First National Bank of Omaha (or in this case their credit card subsidiary, Firstbank Card) is not big enough to offer something legitimate, it’s that they just don’t think they need to. As Firstbank Card owns both JAL and ANA credit cards with the same bonus (and occasional spending bonuses) they compete with no one for Japanese-US travelers. The carriers don’t even compete with each other despite fiercely competing in their home market of Japan and from their competing alliances.

It’s a shame to me that Firstbank Card won the contract for both ANA and JAL and have put no effort into marketing them or turning them into worthwhile cards outside of the endless emails I receive from ANA about nothing promotions. The issuer holds a lot of card contracts. I called in to see what they had and the customer service agent (seriously friendly) discussed how she and her husband have an older Dodge vehicle and may take advantage of the “great bonus” they are offering on the Dodge credit card. It’s $100.

But what’s odd is that a couple of the cards they offer have a reasonable incentive associated with it. They offer 50,000 Best Western points with the BW Premium card and while I would love to tell you how much value that can deliver, the Best Western website is down as I type this. Giving them the benefit of the doubt, let’s say it’s worth $300, just like the Sun Country card that offers 30,000 points though if you go to Mexico at the end of their schedule, that may only be a one-way trip. That’s where the premium offers lie, and by premium, I mean limited to $300-ish. However, even if the bank offered $300 in JAL or ANA miles I would assume we would see a bonus closer to 15-20,000 miles up front. That would be at least reasonably competitive with other Asian carriers though the least generous of them all.

The bank offers a bunch of cards where $50 bonuses make sense, particularly Orvis, Ducks Unlimited, Scheels (all outdoor stores). However, Firstbank Card also offers a pair of China Airlines cards that I have to believe a bigger bank would offer a more meaningful signup bonus (2500 or 7500 points from Firstbank Card).

Don’t Japanese airlines know they can achieve higher revenue through other partners? In turn, if Firstbank had pared back their number of partners and focused on those that may generate a higher volume of business it could be surmised that they may find themselves in a stronger position with higher-end customers as opposed to spreading themselves so thinly across a wide net of niché card products.

If You Want to Fly ANA or JAL on Awards, Don’t get Their Co-Branded Cards

American Express directly offers more points as a signup bonus than the carrier’s own affinity card if you choose to transfer your Membership Rewards Points to ANA. Instead of a 5,000 point bonus after spending on an ANA card with only the possibility to earn and spend those miles on ANA, why not treat other partner card bonuses as an ANA bonus of 100,000 with American Express?

Likewise, you could just go out and get the Bank of America Alaska Airlines card for access to JAL awards at 30,000 miles. Better still, how about one of the new Marriott/SPG cards which will net you as much as 50,000 points to either program with transfer bonuses. British Airways offers an excellent credit card from Chase that if one spent the same (as they would to achieve shopping bonuses with the JAL card) they could use their British Airways Avios to fly farther, faster to and from Japan on JAL.

Why are Chase and American Express willing to give the miles to entice customers when Firstbank (their branded card partner) isn’t? The carriers are clearly willing to sell their miles to banks and partner programs (like hotels) in bulk other than to their specific card partner bank. Why won’t Firstbank Card make a real offer for their customers?

What do you think? Should Firstbank Card offer something real? Are the airlines to blame?

I don’t think it’s the bank, but I think it has something to do with Japan. IIRC, credit cards in Japan, in general, have reward structures that make the stingiest ones (even with 1% return) in the US seem downright generous by comparison.

The one thing going for ANA & JAL credit cards, at least in Japan, is the ability to keep *G or OWS/OWE status just by paying the card’s annual fee (~$100 and up). AFAIK, you do have to earn mid-tier status first, but once you do, you can apply for the ANA Super Flyers Card or JAL Global Club, as long as you’re a resident with decent credit. After that, you get to keep your status as long as your card is in good standing. No flying required.

I am envious of the Japanese version of the card if it came with oneworld Emerald or Star Alliance Gold once entry-level status was achieved. They would be my go-to carrier.

Who’s Gary Leff?

https://viewfromthewing.boardingarea.com/about/

There is nothing wrong with them. They do not mint points endlessly in a never ending treadmill of earn and devalue like US airlines. That is why you can fly ANA business for 75k miles round trip where terrible US business class are 120-140k round trip.

Except that they do, in fact, mint points both directly in the case of ANA through AMEX Membership Rewards and for both carriers in the case of other program tie-ins like hotel point relationships. The AMEX Platinum 100,000 point offer could also be a 100,000 ANA point offer if one were to transfer all of their points there. The SPG card offers 75,000 as a sign-up bonus of which one could transfer all of those points immediately into either program and receive 30,000 points in either program.

It’s not that they don’t mint points, it’s that they don’t do it when the relationship should be most beneficial to them. That’s why I believe it comes down to the bank and not the carrier.

The big thing I think you’re missing here is who the target market is for these cards – expats from Japan with limited credit history. Even the JAL Card’s site alludes to the idea that a limited or non-existent credit history is OK with them, something that larger issuers like Barclay’s and Chase aren’t as willing to take on. I think the fact that this card is marketed for people who are accustomed to (and willing to accept) a sub-par rewards structure by US standards and has laughably low underwriting criteria is the reason we see the low bonuses on these cards. Kind of along the same lines as why we don’t typically see huge bonuses on student cards.

The first question on the JAL USA Card’s FAQ section says it all:

Can I apply for a card without credit history in the U.S.?

Yes. We verify the length of time of employment with the sponsoring company, earnings in home country, as well as, U.S. income and we obtain current contact address in home country and/or the U.S. Therefore, when applying for this card, please provide related information from your home country. Please note, not all requests for credit will be approved.

While the first question is something that I, as a former ex-pat, would have loved to see while we were living abroad I dispute that this card is targeted at newly arrived Japanese ex-pats. Why do I say that? First, because as soon as I signed up for an ANA membership I was inundated with offers for the terrible ANA credit card. They know my home country, they are targeting me with no language that suggests this is primarily for the newly arrived. Second, if Firstbank cards generally offered larger bonuses and this was the sole exception I think your point would hold more merit. However, the China Airlines card bonuses mirror these paltry offers, as do the Scheels card, the Dodge credit card, the Ram credit card (not to be confused with Dodge) and so on. It’s not as though they have a ton of great offers and these are the outliers, but rather they are the norm from this issuer.

Japanese companies are stingy in general. Good luck checking in early at a hotel or getting an upgrade. They are very much rules-based and won’t go outside of policy. Little to no compensation will be given for IROPS. The last offer I got from JAL was a $25 Amazon gift card for booking economy, $50 for premium economy, and $100 for business class.

I agree they are a stickler for rules – I actually filmed the boarding process at HKG whereby the lines were single filed, silent and boarded exactly on time to the second. But that doesn’t mean that they aren’t interested in partnerships that make them money. This could have been a boon for them.

These cards are targeted for Japanese from Japan who are already in the US. As well as Japanese americans.

They are also jal and Ana’s biggerst customer usually, that’s why you get emails even though you are in the us after making mileage accounts.

I am kind of disguised by you wanting more and more miles for just opening a credit? Spend real money and fly!

I’m not too sure if you have flown with them or not but you could tell their customers even in economy are not the same compared to any us carriers.

Their airfare are usually much higher than any US carriers. Again if you actually PAY.

Just get crappy Delta Miles and call a day.

@ihatecheapoidiot – I sense a little animosity that may be unfounded.

1) Another reader has stated that this card is targeted for Japanese expatriates living in the US. Fine, but does that mean there isn’t a market for Americans who want to travel to Asia on their airplanes? I doubt that is the case. If FNBO has the exclusive contract and has decided no American would be interested in getting the card then that is shortsighted on their part. I am one such American (and a former client of the bank no less).

2) They are broadly marketing this to any US-based account which disproves your first statement or they have terrible marketers which is also possible.

3a) I am sorry you are “disguised” by me, but this is the competitive culture of the credit card market in the US. In Spain, bar culture includes free tapas while other parts of the world charge for such snacks – if I am to open a bar in Spain, I either accept the culture or expect a lower turn out at my bar. The same should apply for any market including Japanese entrants to the US credit card system.

3b) Your assumptions, however, are greatly flawed. ANA, for example, has little cost in giving seats away on flights flown on their own metal. One estimate suggests the cost of a business class seat is as little as $30. However, companies make real money from the banks who buy their miles in order to attract customers. While deals are kept secret for proprietary reasons, estimates suggest that the price a bank will pay for airline miles varies between 1.0-1.6¢/mile depending on the carrier and upfront commitment. In this instance that would bring the cost between $50-80 to onboard a customer with either of these two cards. But those card companies are going to earn 2.5% from merchant fees before including ancillary revenue (spillover products, annual fee, interest, etc.).

So when a credit card company offers a 50,000 point bonus after spending $3,000 on the card and paying a $95 annual fee, the cost to the bank is: $330-630 (depending on the rate they pay for the miles). The bank is willing to bet that cost that they will make it up in merchant fees over the life of the customer or other products.

For the airline, they aren’t even giving out enough miles for a roundtrip in business-class so they are looking at earning $500-800 for the sale of their miles plus ongoing sales to the bank to pay out that customer all for the cost of about $30-60.

The airline should want me to open a credit card and spend as much as I can on it, they make out great while it’s the bank carrying all of the risks.

3c) You’re assuming that flying is more profitable to an airline than the mass sale of miles through their loyalty program (it isn’t); that the airline has more to gain from me paying for tickets than they do from me as a credit card customer (they don’t); and that I do not spend big money on their tickets (I did before writing this post, review out soon) and haven’t flown them in the past on cash tickets (I have). You shouldn’t assume, you’re usually wrong.

4) As stated, I just flew with ANA (but not in coach) in business on a cash ticket and you’re right about one thing, it wasn’t cheap. But what does that have to do with their credit card offering? If they had captured my credit card business they could have accrued far more revenue than what I spent on the ticket.

Also, I left Delta years ago and I think you are confusing me with someone else.

What I don’t understand is that, why do you whine and write an article when you are clearly not their targeted audience?

Japanese airlines’ business models are different from us carriers. They try to build customer loyalty by good services, not by giving away worthless miles like us carriers.

I’m sure they will try to get more US based credit holders in the future but for now, those cards offering are seriously aimed for Japanese.

This is a great post.

I’m an AA mileage guy that just moved to Tokyo somewhat permanently. I use the Chase Sapphire card now.

As I will be paid in yen, I’ve been looking at changing to a Japanese card so I don’t have to do currency conversions on purchases and also again when I make a payment.

JAL makes the most sense as I have AA status (at least this year), but I’m willing to jump to ANA if it makes sense. I plan to fly quite a bit on business class.

Any advice on a card??